Introduction:

As we usher in the new year, the world of real estate and homeownership is set to witness a transformative change with the 2024 loan limit increases. This blog aims to provide a comprehensive guide to understanding the implications of the increased loan limits for conforming, FHA, and VA loans, offering valuable insights for prospective homebuyers navigating the evolving landscape.

Loan Limit Increases Conforming Loans:

Conforming loans, those that adhere to the limits set by Fannie Mae and Freddie Mac, are in for an upgrade in 2024. The increased loan limits mean that borrowers can secure larger loans while still enjoying the benefits of conforming loan terms. This expansion is poised to empower homebuyers, particularly in areas with higher housing costs, by providing more financial flexibility and expanding their choices in the housing market. (2024 Loan Limits)

FHA Loans:

The Federal Housing Administration (FHA) plays a crucial role in assisting homebuyers with more flexible financing options, and 2024 brings positive news for FHA loan seekers. The higher FHA loan limits open doors for a broader range of borrowers, allowing them to access affordable financing for homes in various markets. This change is expected to enhance affordability and inclusivity in homeownership, aligning with the FHA’s mission to support a diverse range of buyers. (2024 FHA Loan Limits)

VA Loans:

The VA loan program has consistently supported veterans, active-duty service members, and eligible spouses. Since 2020, eligible military borrowers with full entitlement—having no other active VA loans—no longer face loan limits. In 2024, elevated VA loan limits further amplify this support, empowering veterans with increased purchasing power. The expanded eligibility thresholds enable more military families to benefit from favorable terms, emphasizing the VA loan program’s steadfast commitment to acknowledging and honoring their service. (Read More)

What Does It Mean for Homebuyers?

Prospective homebuyers stand to gain significantly from the 2024 loan limit increases. The expanded limits across conforming, FHA, and VA loans translate into increased homebuying power. This can be particularly advantageous for those looking to enter the real estate market, upgrade their current homes, or explore properties in regions with higher housing costs.

Advice for Homebuyers:

As a potential homebuyer in 2024, staying informed about the loan limit increases is crucial. Consult with mortgage professionals to understand how these changes can benefit you. Take advantage of the expanded loan limits to explore a wider range of homes and secure more favorable financing terms.

Conclusion:

The 2024 loan limit increases for conforming, FHA, and VA loans signal a positive shift in the housing market, offering opportunities and flexibility for aspiring homeowners. Whether you’re looking to enter the market, upgrade your current residence, or utilize VA loan benefits, these changes create a promising landscape for realizing your homeownership dreams in the coming year. Stay informed, explore your options, and embark on your homeownership journey with confidence.

The post 2024 Brings Homeownership Opportunities: Significant Loan Limit Increases Unveiled! appeared first on Scenic Oaks Funding.

]]>

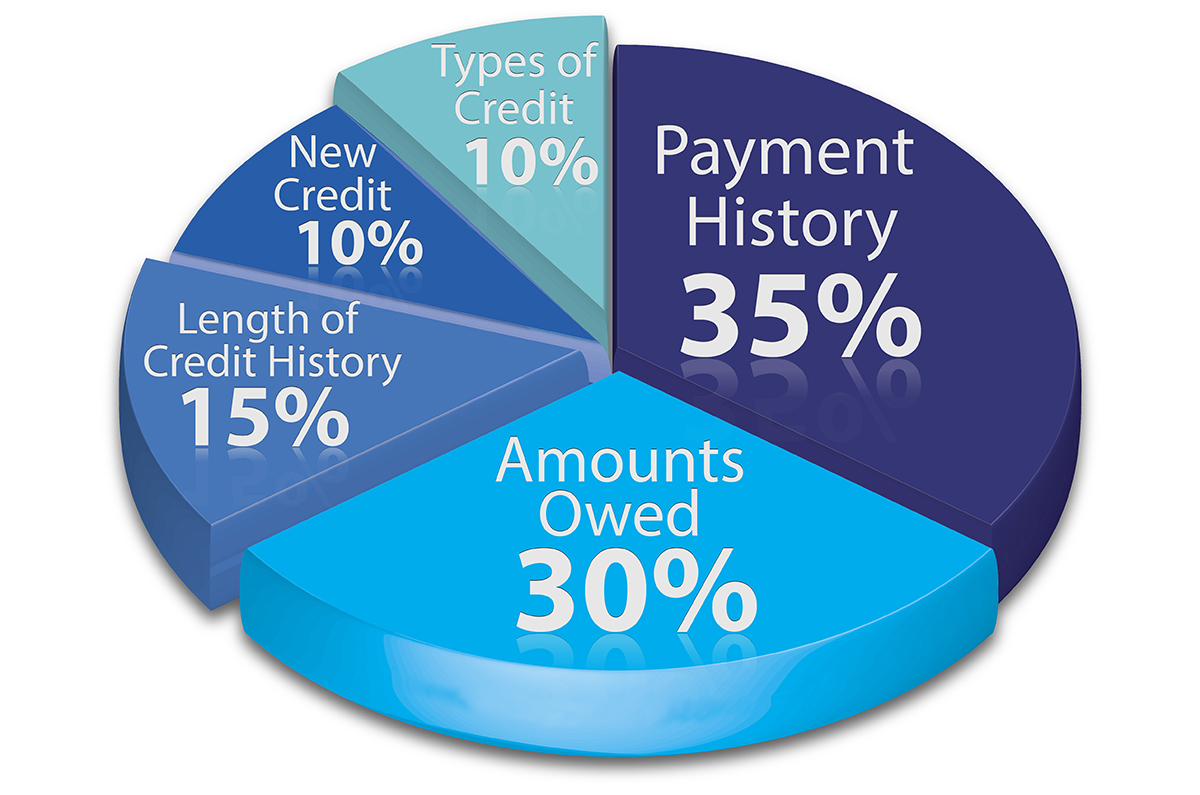

The post Credit Comeback: Your Guide to Boosting Your Credit Score appeared first on Scenic Oaks Funding.

]]>

Mortgage insurance, while a useful tool for homeowners to get into a home sooner, often becomes an unnecessary cost as you build equity in your home. Whether it’s Private Mortgage Insurance (PMI) for conventional loans or Mortgage Insurance Premiums (MIP) for FHA loans, many homeowners look forward to the day they can cancel this extra expense. Here’s a comprehensive guide on how to cancel your mortgage insurance, freeing up money in your monthly budget.

Understand What You Have: PMI vs. MIP

Private Mortgage Insurance (PMI)

- PMI is typically required when you have a conventional loan and make a down payment of less than 20% of the home’s purchase price. PMI protects the lender in case you default on your loan.

Mortgage Insurance Premium (MIP)

- MIP is required for all FHA loans, regardless of your down payment. There are two types of MIP: upfront MIP, paid at closing, and annual MIP, paid monthly.

Cancelling PMI

- Automatic Termination

- Under the Homeowners Protection Act, your lender must automatically terminate PMI on the date your principal balance is scheduled to reach 78% of the original value of your home, as long as you are current on your payments.

- Requesting Early Cancellation

- You can request to cancel PMI when your mortgage balance reaches 80% of the original value of your home. Here’s how:

- Check Your Balance: Review your mortgage statement to see your current balance. Use your original purchase price as the benchmark for calculating 80%.

- Understand Your Lender’s Requirements: Lenders may have specific requirements for PMI cancellation, such as a good payment history and no liens on the property

- Get a Home Appraisal: If you believe your home has appreciated in value, you may reach the equity threshold sooner. However, you’ll likely need a professional appraisal to prove this to your lender, which you will have to pay for.

- Submit a Request in Writing: Send a written request to your lender asking for PMI cancellation. Include your account number and any evidence of your home’s value, if applicable.

- Continue Payments: Continue making your regular mortgage payments while your request is processed.

- You can request to cancel PMI when your mortgage balance reaches 80% of the original value of your home. Here’s how:

Cancelling MIP on FHA Loans

Cancelling MIP is more challenging and depends on when your loan was originated:

- Loans Originated Before June 3, 2013: You can request to cancel MIP when your loan-to-value ratio reaches 78%.

- Loans Originated After June 3, 2013: For loans with an initial down payment of less than 10%, MIP cannot be cancelled and is required for the life of the loan. For initial down payments of 10% or more, MIP is required for 11 years.

Unfortunately, the only way to eliminate MIP on newer FHA loans with a down payment of less than 10% is by refinancing into a conventional loan once you’ve reached 20% equity.

Refinancing as an Alternative

If you’re not eligible to cancel your mortgage insurance through the methods mentioned above, refinancing could be a viable option. Refinancing your mortgage to a conventional loan might eliminate the need for PMI if you have at least 20% equity in your home. However, consider the closing costs associated with refinancing to ensure it’s a financially beneficial move.

Conclusion

Cancelling mortgage insurance can potentially save you hundreds to thousands of dollars annually, but it requires an understanding of your loan type, equity, and the rules that apply. By following the steps outlined above, you can navigate the process more smoothly and work towards removing this extra monthly expense. As always, consult with your lender or a financial advisor to understand your specific situation and the best course of action for your financial future.

The post Smart Moves: Cancelling Mortgage Insurance appeared first on Scenic Oaks Funding.

]]>